If you’re new to investing, index funds are one of the easiest and safest ways to get started. You don’t need to be a finance expert or constantly track the stock market. Let’s break it down in simple terms.

✅ What Is an Index?

An index is a group of selected companies that represent a portion of the stock market. For example:

Nifty 50 – tracks the top 50 companies listed on the NSE (India)

Sensex – tracks 30 major companies on the BSE

S&P 500 – tracks 500 of the biggest companies in the U.S.

These indexes show how the overall market (or part of it) is performing.

Table of Contents

📦 What Is an Index Fund?

An index fund is a type of mutual fund or ETF (exchange-traded fund) that simply copies an index. It invests in the same companies in the same proportion.

For example: If you invest in a Nifty 50 Index Fund, your money is automatically spread across the top 50 companies in India—like Reliance, Infosys, HDFC Bank, etc.

💡 Why Are Index Funds Great for Beginners?

Low cost: No fund manager trying to beat the market = lower fees

Low risk: Diversified across many companies = less chance of loss

No stress: You don’t need to research or time the market

Long-term growth: Historically, markets tend to go up over time

🔍 Active Funds vs. Index Funds (Quick Comparison)

Feature

Active Fund

Index Fund

Managed by Expert

Yes

No

Tries to Beat Market

Yes

Just matches the market

Fees (Expense Ratio)

High (1%–2%)

Low (0.1%–0.5%)

Risk

Medium to High

Lower

Best For

Risk-takers or experts

Beginners & long-term

📝 Real-Life Analogy

Think of an index fund like a thali meal at a restaurant.

You get a little of everything on one plate, instead of ordering individual dishes. It’s easier, more balanced, and you don’t need to be a chef to enjoy it.

Why Invest in Index Funds? Key Benefits Explained

Index funds have become one of the most popular investment choices worldwide—and for good reason. Unlike traditional mutual funds that are actively managed by fund managers, index funds simply aim to replicate the performance of a market index like the Nifty 50 or Sensex. This passive strategy brings several powerful benefits, especially for beginner and long-term investors.

One of the biggest advantages of index funds is their low cost. Because there’s no active decision-making or stock picking involved, fund management fees (known as expense ratios) are significantly lower than regular mutual funds. This means more of your money stays invested and continues to grow over time.

Index funds also offer instant diversification. Instead of buying shares of just one company (which can be risky), your money is automatically spread across dozens or even hundreds of top companies in the index. This reduces the risk of losing money due to the poor performance of a single company. If one company does badly, it’s often balanced out by others doing well.

Another huge benefit is simplicity and ease of use. You don’t need to time the market, pick winning stocks, or follow financial news daily. Index funds are designed to mirror the market, so they naturally grow over time as the economy grows. This makes them ideal for long-term wealth building, especially through SIPs (Systematic Investment Plans), where you invest small amounts every month.

Finally, research shows that over the long run, most actively managed funds fail to beat the market. So rather than trying to guess which fund manager or stock will outperform, index fund investors just ride the wave of the market itself—slow, steady, and consistent.

In short, index funds are cost-effective, low-risk, and stress-free. Whether you’re saving for retirement, a big goal, or just looking to grow your wealth safely, index funds offer a smart, beginner-friendly path into the world of investing.

How Do Index Funds Work?

Index funds work on a simple but powerful idea: instead of trying to beat the market, they aim to match the market’s performance. They do this by investing in all the stocks that make up a specific market index, in the same proportion as the index itself.

Let’s say you invest in a Nifty 50 index fund. The fund will take your money and spread it across the top 50 companies in India, like Reliance, TCS, Infosys, HDFC Bank, etc.—exactly the way they’re weighted in the Nifty 50 index. If Reliance makes up 10% of the Nifty 50, then 10% of your money goes into Reliance shares, and so on. This way, the fund mirrors the index.

Here’s the step-by-step breakdown of how index funds work:

You invest money (either as a one-time lump sum or monthly SIP).

The fund manager takes your money and buys the same stocks that are in the index.

When the index goes up or down, the value of your fund also goes up or down accordingly.

You can track the fund’s performance daily or monthly—it will closely follow the index.

You can sell your investment anytime (subject to exit loads or tax rules).

Since index funds are passively managed, the fund manager doesn’t try to pick “hot” stocks or predict market movements. This keeps costs low, and the performance tends to match the market average, which over the long term, can be better than most actively managed funds.

So in short, index funds are like a “copy-paste” version of the market—simple, stable, and designed for long-term, low-effort investing.

Step-by-Step Guide to Investing in Index Funds

Investing in index funds is easier than you might think—even if you have no prior experience or don’t have a demat account. Here’s a full walkthrough to help you get started with confidence.

✅ Step 1: Understand the Two Types of Index Funds

There are two ways to invest in index funds:

Index Mutual Funds – You can invest directly from mutual fund platforms or apps.

Index ETFs (Exchange-Traded Funds) – These require a demat and trading account because ETFs are traded like stocks on the stock exchange.

📌 If you’re a beginner without a demat account, start with index mutual funds.

✅ Step 2: Complete KYC (Know Your Customer)

Before you can invest in any mutual fund in India, you must complete KYC.

You’ll need:

PAN card

Aadhaar card

Bank account with IFSC code

A selfie (for verification on most apps)

Signature (digital or scanned)

Most platforms let you complete e-KYC online in a few minutes.

✅ Step 3: Choose an Investment Platform

Here are some reliable platforms/apps to invest in index mutual funds:

Groww

Zerodha Coin

ET Money

Paytm Money

Kuvera

Direct AMC websites (like ICICI, HDFC, UTI, etc.)

🔎 Tip: Choose direct plans instead of regular plans. Direct plans have lower expense ratios(fewer fees), which means better returns over time.

✅ Step 4: Select the Right Index Fund

Popular index funds to start with:

Nifty 50 Index Fund

Sensex Index Fund

Nifty Next 50 Index Fund

S&P 500 Index Fund (for exposure to US markets)

When choosing a fund, compare:

Expense Ratio – Lower is better (aim for < 0.5%)

Tracking Error – Lower means the fund mirrors the index more accurately

Fund House Reputation – Go with trusted names (HDFC, UTI, ICICI, Nippon, etc.)

✅ Step 5: Choose SIP or Lump Sum Investment

You can invest:

SIP (Systematic Investment Plan) – Invest a fixed amount monthly (as low as ₹100–₹500)

Lump Sum – Invest a larger one-time amount (₹5,000+)

💡 For beginners, SIP is the best way to build discipline and benefit from rupee-cost averaging (buying more units when prices are low).

✅ Step 6: Monitor Your Investment (But Don’t Panic)

Index funds are long-term investments. You don’t need to check them daily.

Instead:

Review your portfolio once every 6–12 months

Track if the fund is consistently following the index

Avoid switching funds too often unless there’s a long-term performance issue

✅ Step 7: Know the Exit Rules & Tax Implications

Exit Load: Some funds charge a fee if you sell within 1 year (usually 1%)

Capital Gains Tax:

Short-term (<1 year): 15% tax

Long-term (>1 year): 10% tax on gains above ₹1 lakh/year

Keep this in mind while planning withdrawals.

How Much Money Do You Need to Start Investing?

One of the biggest myths about investing is that you need to be rich to begin. In reality, you can start investing in index funds in India with as little as ₹100. That’s less than what many people spend on coffee or snacks in a day!

If you’re investing in index mutual funds, most fund houses offer SIP (Systematic Investment Plan) options starting from:

₹100 to ₹500 per month

This means you can build wealth slowly, without stressing your budget.

For lump sum investments, the minimum is usually around ₹5,000, but this can vary depending on the fund.

🧠 Pro tip: Don’t wait to have ₹50,000 or ₹1 lakh in hand. Start small with SIPs. Time in the market is more powerful than timing the market.

💰 Example: Monthly SIP of ₹500

If you invest ₹500/month in an index fund for 10 years

And it grows at an average annual return of 12%

You’ll end up with ₹1.15 lakh from just ₹60,000 invested!

That’s the power of compound growth.

🏦 Do You Need a Demat Account?

For index mutual funds: ❌ No Demat account needed

For ETFs (index funds traded on the stock market): ✅ Demat required

So if you’re starting with mutual fund-based index funds via apps like Groww, Paytm Money, or Kuvera, you don’t need any special trading setup—just basic KYC and a savings account.

🧾 What About Other Costs?

Expense Ratio: Very low (often between 0.1% and 0.5%)

No brokerage fees for mutual funds

No hidden charges if you choose a direct plan

Exit load only if you sell before 1 year (usually 1%)

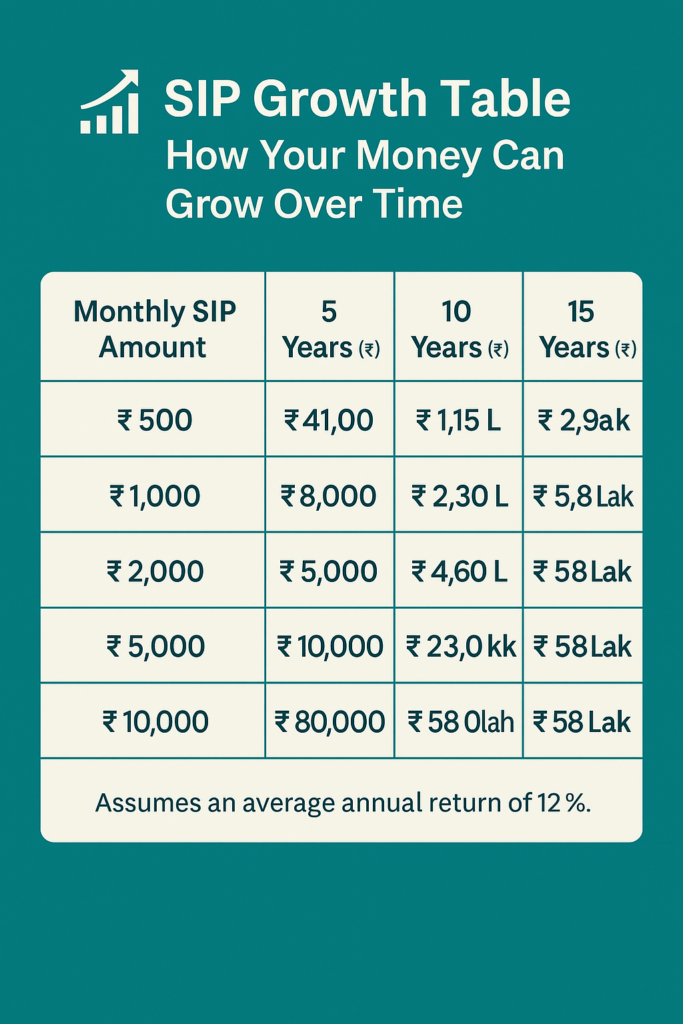

SIP Growth Table: How Your Money Can Grow Over Time

Monthly SIP Amount

5 Years (₹)

10 Years (₹)

15 Years (₹)

₹500

₹41,000

₹1.15 Lakh

₹2.90 Lakh

₹1,000

₹82,000

₹2.30 Lakh

₹5.80 Lakh

₹2,000

₹1.64 Lakh

₹4.60 Lakh

₹11.6 Lakh

₹5,000

₹4.10 Lakh

₹11.5 Lakh

₹29 Lakh

₹10,000

₹8.20 Lakh

₹23 Lakh

₹58 Lakh

💡 Assumes an average annual return of 12%, which is realistic for index funds over the long term.

SIP TABLE

🧠 What This Means

You don’t need to wait to earn big.

Even ₹500/month consistently can grow into lakhs over time.

The longer you stay invested, the more your money grows—thanks to compound interest.

Index Funds vs. Actively Managed Funds: What’s the Difference?

The key difference between index funds and actively managed funds lies in how they are managed. Index funds are passively managed, which means they aim to copy the performance of a specific market index like Nifty 50 or Sensex. Fund managers don’t pick stocks; they simply invest in all the companies listed in the index in the same proportion. This approach keeps costs low, risk moderate, and performance consistent with the market. It’s ideal for long-term investors who want steady growth without paying high fees.

On the other hand, actively managed funds have professional fund managers who try to beat the market by researching and selecting specific stocks they believe will perform better. While this sounds appealing, it comes with higher fees, greater risk, and no guarantee of better returns. In fact, studies show that many active funds fail to outperform index funds over the long run. For most beginners and even experienced investors, index funds offer a simpler, cheaper, and more reliable way to build wealth gradually.

Comparison Table: Index Funds vs. Actively Managed Funds

Feature

Index Funds

Actively Managed Funds

Management Style

Passive (copies an index)

Active (fund manager selects stocks)

Goal

Match market performance

Beat the market

Expense Ratio (Fees)

Low (0.1% – 0.5%)

High (1% – 2.5%)

Risk Level

Moderate (market-wide exposure)

Higher (depends on fund manager’s choices)

Returns (Long-Term)

Consistent with market averages

May outperform or underperform the market

Simplicity

Easy to understand and invest in

Requires research and monitoring

Best For

Beginners & long-term passive investors

Experienced investors willing to take more risk

Top Index Funds to Consider in 2025 (and What Makes Them Special)

Investing in the right index fund can make a big difference in the long run. Here are some of the best index funds to consider in 2025, along with what makes each one stand out:

1. Nippon India Nifty 50 Index Fund (Direct Plan)

🔹 Unique Qualities:

Tracks the Nifty 50, India’s top 50 companies

One of the lowest expense ratios in the category (~0.20%)

Great for beginners looking for exposure to India’s overall economy

Long-term consistent performance with high liquidity

2. HDFC Index Fund – Nifty 50 Plan (Direct)

🔹 Unique Qualities:

Backed by HDFC—strong reputation and fund management history

Simple, no-frills fund tracking the Nifty 50 index

Ideal for investors seeking stability, low cost, and long-term growth

Known for very low tracking error over time

3. UTI Nifty Next 50 Index Fund (Direct)

🔹 Unique Qualities:

Tracks the Nifty Next 50, which includes the “next in line” companies after Nifty 50

Offers high growth potential with slightly more volatility

Great for diversifying beyond just the top companies

Popular among young investors aiming for long-term capital appreciation

4. ICICI Prudential Nifty 100 Index Fund (Direct)

🔹 Unique Qualities:

Covers top 100 companies, offering broader exposure than Nifty 50

Balanced between stability and growth

Good choice if you want to stay in large-cap but diversify a bit more

Reliable brand and strong fund management

5. Motilal Oswal S&P 500 Index Fund (Direct)

🔹 Unique Qualities:

Gives exposure to top 500 U.S. companies like Apple, Google, Amazon

Ideal for international diversification without needing a forex account

Great hedge against currency depreciation (₹ vs $)

Suitable for long-term investors who want global growth potential

6. Parag Parikh Flexi Cap Fund (Bonus Mention – Hybrid Approach)

🔹 Unique Qualities:

Not a pure index fund, but combines Indian and U.S. stocks actively

Suitable for investors looking for a mix of passive + active exposure

One of the most popular low-risk hybrid funds with steady returns

Common Mistakes to Avoid When Investing in Index Funds

Index funds are beginner-friendly, but that doesn’t mean they’re foolproof. Many new investors make small mistakes that can reduce returns or lead to disappointment. Here are some of the most common (and realistic) mistakes to avoid when investing in index funds—especially if you’re just starting out:

1. Expecting Quick Profits

Many beginners invest expecting big returns in a few months. But index funds are not meant for short-term gains. They’re designed for steady, long-term growth over 5–10+ years. If you check your returns daily or expect your ₹10,000 to become ₹20,000 in 6 months, you’ll likely be disappointed. Patience is the key—stick with it.

2. Stopping SIPs When the Market Falls

A common panic move: markets fall, and investors stop their SIPs or withdraw. But in reality, market dips are the best time to invest more because you’re buying units at a lower price. Over time, this improves your average cost and boosts long-term returns. So don’t fear red numbers—they’re temporary.

3. Choosing High Expense Ratio Funds

Not all index funds are created equal. Some charge more than others—even for the same index. A higher expense ratio (fees) eats into your returns silently over years. Always choose direct plans with low expense ratios (preferably below 0.5%).

4. Ignoring Tracking Error

Tracking error is how closely a fund follows its index. A high tracking error means the fund isn’t accurately matching the index’s returns. Many new investors miss this detail. Before you invest, check the tracking error on the AMC website or financial platforms—lower is better.

5. Over-diversifying with Too Many Index Funds

It’s tempting to buy multiple index funds (like Nifty 50, Nifty 100, Nifty Next 50, Sensex, etc.) thinking it reduces risk. But these funds often hold similar stocks, leading to overlap. It’s smarter to invest in 1–2 well-chosen funds (like one India-focused and one global fund) rather than 5 funds doing the same thing.

6. Not Reviewing Investments Periodically

Even though index funds are passive, you shouldn’t invest and forget forever. Every 6–12 months, check if:

Your fund is performing close to the index

Tracking error or expense ratio hasn’t changed drastically

Your goals or risk tolerance has changed

7. Investing Without a Goal or Plan

Many people invest just because they heard it’s good—but having no goal (like retirement, buying a home, etc.) makes it hard to stay committed. Set a goal, decide how much you can invest monthly, and stick with it. It gives you clarity and motivation to stay consistent.

🧠 Final Thought

Index funds are simple, but your success still depends on discipline, awareness, and patience. Avoid these mistakes, and you’ll be way ahead of most new investors.

Recommended Tools and Platforms for Index Fund Investors

Whether you’re just starting or looking to manage your investments smarter, using the right tools and platforms makes a big difference. Here’s a breakdown of the best apps, websites, and tools that make investing in index funds easier, safer, and more efficient in 2025:

📱 Top Investment Platforms in India

These platforms allow you to invest in direct mutual fund index funds (without needing a demat account):

Platform

Key Features

Groww

User-friendly, fast KYC, tracks returns, SIP setup, app + web support

Zerodha Coin

Great for those already using Zerodha, clean interface, no commission

ET Money

Easy tracking, auto-SIP feature, portfolio insights, useful for goal planning

Kuvera

100% free direct fund investing, great for family portfolio tracking

Paytm Money

Easy onboarding, supports stocks + mutual funds, decent for new investors

💡 Tip: Always choose the “Direct Plan” when investing—this avoids middlemen and gives higher returns due to lower fees.

📊 Best Research & Comparison Tools

Want to compare funds before investing? Use these free tools:

Tool/Website

Use For

Value Research Online

Detailed fund comparisons, past performance, expense ratio, rating

Morningstar India

Professional analysis, portfolio breakdown, risk metrics

Screener.in

For exploring index-linked stocks if you want to go deeper

Moneycontrol

Quick news, NAV updates, fund reviews

🛠️ Other Helpful Tools for SIP Planning & Tracking

Tool

What It Does

SIP Calculator (ET Money / Groww)

Helps you estimate how much you’ll accumulate based on monthly investment

Goal Planner (Kuvera / Paytm Money)

Set a financial goal and calculate how much SIP is needed

Tickertape or Finology

Fund insights, ratios, and other financial metrics

🧠 Final Advice:

Start with one simple platform (like Groww or Kuvera), track your investments monthly, and avoid chasing returns. Use calculators and comparison tools to plan smarter, not harder.

CS Annu Sharma is a qualified and experienced professional in the field of Company Secretarial and Legal activities. With an impressive academic background and relevant certifications, she has demonstrated exceptional expertise and dedication in her career.Education:Qualified Company Secretary (CS) from the Institute of Company Secretaries of India (ICSI).

Graduate in Law from Indraparasth Law College, enabling a strong legal foundation in her professional journey.

Graduate in Commerce from Delhi University, providing her with a comprehensive understanding of financial and business concepts.

Certifications:Certified CSR Professional from the Institute of Company Secretaries of India (ICSI), showcasing her commitment to corporate social responsibility and ethical business practices.Work Experience:

She possesses an extensive and diversified work experience of more than 7 years, focusing on Secretarial and Legal activities. Throughout her career, she has consistently showcased her ability to handle complex corporate governance matters and legal compliance with utmost efficiency and precision.Current Position:

Currently, Mrs. Annu holds a prominent position in an NSE Listed Entity, namely Globe International Carriers Limited, based in Jaipur. As a key member of the organization, she plays a vital role in ensuring compliance with regulatory requirements, advising the management on corporate governance best practices, and safeguarding the company's interests.Professional Attributes:Thorough knowledge of corporate laws, regulations, and guidelines in India, enabling her to provide strategic insights and support in decision-making processes.Expertise in handling secretarial matters, including board meetings, annual general meetings, and other statutory compliances.

Proficiency in drafting legal documents, contracts, and agreements, ensuring accuracy and adherence to legal requirements.Strong understanding of corporate social responsibility and its impact on sustainable business practices.Excellent communication and interpersonal skills, enabling effective collaboration with various stakeholders, both internal and external.Personal Traits:

Mrs. Annu Khandelwal is known for her dedication, integrity, and commitment to maintaining the highest ethical standards in her professional conduct. Her meticulous approach to work and attention to detail make her an invaluable asset to any organization she is associated with.Conclusion:

Cs Annu 's profile exemplifies a highly qualified and accomplished Company Secretary, well-versed in legal matters and corporate governance. With her wealth of experience and commitment to excellence, she continues to contribute significantly to the success and growth of the organizations she serves.